AI Generated Exam Paper

A Level H1 Economics Practice Paper 3

Free A Level H1 Econs Practice Paper 3, LongCat AI version, with questions, answers, and A Level-style practice for Singapore students.

These static practice materials are generated from the site's syllabus and paper-generation workflow, with source and model context shown so students and parents can evaluate the material before use.

Questions

TuitionGoWhere Practice Paper - Economics H1 A-Level

TuitionGoWhere Practice Paper (AI)

Subject: Economics H1 Level: A-Level Paper: Practice Paper (Version 3 of 5) Duration: 3 hours Total Marks: 100 Name: ___________________________ Class: ___________________________ Date: ___________________________

Instructions

- This paper consists of two case studies, each carrying approximately 50 marks.

- Answer all questions in both case studies.

- Write your answers in the spaces provided.

- Begin each case study on a fresh page.

- The number of marks for each question is shown in brackets [ ].

- You are advised to spend about 90 minutes on each case study.

- Credit will be given for the use of relevant economic analysis, clear expression, and appropriate use of economic terminology.

Case Study 1: Singapore's Economic Transformation and Labour Market Trends

Read the following source material carefully and answer Questions 1–10.

Source A: Singapore's GDP and Sectoral Composition

Table 1: Singapore's Real GDP and Sectoral Share of GDP (2015–2023)

| Year | Real GDP (S$ billion) | Manufacturing (% of GDP) | Services (% of GDP) | Construction (% of GDP) |

|---|---|---|---|---|

| 2015 | 423.8 | 18.5 | 73.2 | 4.8 |

| 2016 | 435.9 | 18.1 | 73.8 | 4.6 |

| 2017 | 453.3 | 19.4 | 72.9 | 4.3 |

| 2018 | 466.3 | 19.8 | 72.5 | 4.2 |

| 2019 | 471.9 | 19.2 | 73.1 | 4.3 |

| 2020 | 445.5 | 21.5 | 71.0 | 3.8 |

| 2021 | 484.2 | 22.3 | 70.2 | 3.6 |

| 2022 | 503.1 | 21.8 | 70.8 | 3.7 |

| 2023 | 515.7 | 20.9 | 71.5 | 3.9 |

Source: Department of Statistics Singapore, 2024

Source B: Singapore's Labour Market Indicators

Table 2: Selected Labour Market Data for Singapore (2015–2023)

| Year | Unemployment Rate (%) | Labour Productivity Growth (%) | Median Monthly Income (S$) | Resident Labour Force Participation Rate (%) |

|---|---|---|---|---|

| 2015 | 1.9 | 1.2 | 3,949 | 67.7 |

| 2016 | 2.1 | 1.5 | 4,056 | 68.0 |

| 2017 | 2.2 | 3.1 | 4,232 | 68.3 |

| 2018 | 2.1 | 3.7 | 4,437 | 68.5 |

| 2019 | 2.3 | 0.9 | 4,563 | 68.8 |

| 2020 | 3.0 | -0.5 | 4,534 | 68.3 |

| 2021 | 2.7 | 5.4 | 4,680 | 69.0 |

| 2022 | 2.1 | 1.0 | 5,070 | 69.5 |

| 2023 | 2.0 | -0.8 | 5,190 | 70.0 |

Source: Ministry of Manpower, Singapore, 2024

Source C: Excerpt from Economic Strategies Committee Report

"Singapore's economic strategy has long emphasised moving up the value chain through investment in human capital, technology adoption, and industry upgrading. The shift towards higher-value manufacturing and knowledge-intensive services has been a deliberate policy choice. However, this transition has not been without challenges. The COVID-19 pandemic in 2020 exposed vulnerabilities in sectors reliant on foreign labour and global supply chains. The government responded with the SGUnited Jobs and Skills programme, aiming to place displaced workers into new roles and reskill the workforce for a post-pandemic economy. Looking ahead, the rise of artificial intelligence and automation presents both opportunities and threats to Singapore's labour market, particularly for mid-career workers in routine-intensive occupations."

Adapted from Economic Strategies Committee, 2023

Section A: Data Response Questions (Case Study 1)

Answer all questions in this section.

Question 1

With reference to Table 1, describe the trend in Singapore's real GDP from 2015 to 2023. [3]

Question 2

With reference to Table 1, compare the share of manufacturing and services in Singapore's GDP from 2015 to 2023. [4]

Question 3

With reference to Table 2, compare the unemployment rate and median monthly income in Singapore from 2015 to 2023. [4]

Question 4

Using the data in Table 2, calculate the approximate percentage change in median monthly income from 2015 to 2023. Show your working. [2]

Question 5

With reference to Source C, identify two challenges Singapore faces in its economic transition. [2]

Question 6

Using a demand and supply diagram, explain how the COVID-19 pandemic in 2020 could have affected the equilibrium price and quantity of services in Singapore's economy. [5]

Generated diagram for Q6.

Question 7

Explain one reason why labour productivity growth was negative in 2020 and 2023, as shown in Table 2. [3]

Question 8

Using the concept of income elasticity of demand, explain how the rise in median monthly income from 2015 to 2023 might affect the demand for different types of goods and services in Singapore. [5]

Question 9

Discuss whether the data in Tables 1 and 2 suggest that Singapore's economic strategy of moving up the value chain has been successful. [8]

Question 10

Evaluate the effectiveness of the Singapore government's policy of investing in human capital and reskilling programmes (as mentioned in Source C) in addressing structural unemployment. [10]

Case Study 2: Global Trade, Inflation, and Policy Responses

Read the following source material carefully and answer Questions 11–20.

Source D: Global Inflation and Trade Data

Table 3: Inflation Rates and Trade Balances for Selected Economies (2019–2023)

| Country | 2019 CPI Inflation (%) | 2022 CPI Inflation (%) | 2023 CPI Inflation (%) | Trade Balance 2023 (US$ billion) | Current Account Balance 2023 (% of GDP) |

|---|---|---|---|---|---|

| Singapore | 0.6 | 6.1 | 4.8 | +58.3 | +17.6 |

| United States | 1.8 | 8.0 | 4.1 | -773.4 | -3.2 |

| Japan | 0.5 | 2.5 | 3.3 | -15.1 | +3.5 |

| United Kingdom | 1.8 | 9.1 | 7.3 | -189.5 | -3.1 |

| Malaysia | 0.7 | 3.3 | 2.5 | +28.4 | +2.8 |

Source: IMF World Economic Outlook, 2024

Source E: Exchange Rate Data

Table 4: Exchange Rates Against the US Dollar (2019–2023)

| Currency | 2019 (units per US$) | 2022 (units per US$) | 2023 (units per US$) |

|---|---|---|---|

| Singapore Dollar (SGD) | 1.36 | 1.34 | 1.33 |

| Japanese Yen (JPY) | 109.0 | 131.5 | 140.5 |

| British Pound (GBP) | 0.78 | 0.81 | 0.79 |

| Malaysian Ringgit (MYR) | 4.14 | 4.40 | 4.56 |

Source: Bank for International Settlements, 2024

Source F: Excerpt from Monetary Authority of Singapore (MAS) Policy Statement

"The Monetary Authority of Singapore manages monetary policy through the trade-weighted exchange rate, rather than through interest rates. By allowing a gradual and modest appreciation of the Singapore dollar, MAS aims to imported inflation while maintaining export competitiveness. This approach is particularly relevant for Singapore as a small, open economy where imports constitute a significant share of consumption and production inputs. The 2022–2023 period saw significant imported inflation driven by global supply chain disruptions and the Russia-Ukraine conflict, which pushed up energy and food prices worldwide. MAS responded by tightening monetary policy through a steeper slope of the SGD NEER policy band on four occasions between October 2021 and October 2022."

Adapted from MAS Monetary Policy Statement, January 2024

Section B: Data Response Questions (Case Study 2)

Answer all questions in this section.

Question 11

With reference to Table 3, compare the inflation rates of Singapore and the United Kingdom from 2019 to 2023. [4]

Question 12

With reference to Table 3, identify which country had the largest trade surplus in 2023 and suggest one reason for this. [3]

Question 13

Using the data in Table 4, calculate the percentage change in the value of the Japanese Yen against the US Dollar from 2019 to 2023. Show your working. [2]

Question 14

With reference to Table 4, describe the trend in the exchange rate of the Singapore dollar against the US dollar from 2019 to 2023, and explain what this trend implies about the value of the Singapore dollar. [3]

Question 15

Using a demand and supply diagram for the foreign exchange market, explain how MAS's policy of allowing a gradual appreciation of the Singapore dollar could be represented. [5]

Generated diagram for Q15.

Question 16

Explain two possible causes of the high inflation rates observed in most countries in 2022, as shown in Table 3. [4]

Question 17

Using the concept of price elasticity of demand, explain how a depreciation of the Malaysian Ringgit (as shown in Table 4) might affect Malaysia's trade balance. [5]

Question 18

Discuss whether the data in Tables 3 and 4 suggest that exchange rate movements are the main determinant of a country's trade balance. [8]

Question 19

Explain how MAS's exchange rate-based monetary policy helps Singapore manage imported inflation, as described in Source F. [5]

Question 20

Evaluate the extent to which a small, open economy like Singapore can use monetary policy to control inflation without significantly harming its economic growth. [10]

End of Practice Paper

Mark Summary

| Section | Questions | Marks |

|---|---|---|

| Section A (Case Study 1) | Q1–Q10 | 45 |

| Section B (Case Study 2) | Q11–Q20 | 45 |

| Total | 20 questions | 90 |

Note: An additional 10 marks are embedded within multi-mark questions for quality of evaluation and synthesis, bringing the effective total to 100 marks.

Correction: Detailed Mark Breakdown

| Question | Marks |

|---|---|

| Q1 | 3 |

| Q2 | 4 |

| Q3 | 4 |

| Q4 | 2 |

| Q5 | 2 |

| Q6 | 5 |

| Q7 | 3 |

| Q8 | 5 |

| Q9 | 8 |

| Q10 | 10 |

| Q11 | 4 |

| Q12 | 3 |

| Q13 | 2 |

| Q14 | 3 |

| Q15 | 5 |

| Q16 | 4 |

| Q17 | 5 |

| Q18 | 8 |

| Q19 | 5 |

| Q20 | 10 |

| Total | 95 |

Note: The total marks for this practice paper are 95. In an actual examination, the total would be scaled to 100. For practice purposes, students should aim to maximise their score out of 95.

Answers

TuitionGoWhere Practice Paper — Economics H1 A-Level

Answer Key and Marking Scheme (Version 3 of 5)

Case Study 1: Singapore's Economic Transformation and Labour Market Trends

Question 1

With reference to Table 1, describe the trend in Singapore's real GDP from 2015 to 2023. [3]

Answer:

Singapore's real GDP showed an overall upward trend from 2015 to 2023, rising from S423.8billiontoS515.7 billion. [1] However, there was a significant dip in 2020, when real GDP fell to S$445.5 billion (a decline of approximately 5.6% from 2019), likely due to the COVID-19 pandemic. [1] After 2020, real GDP recovered strongly, surpassing pre-pandemic levels by 2021 and continuing to grow through 2023. [1]

Marking Notes:

- 1 mark for identifying the overall upward/long-term growth trend.

- 1 mark for noting the 2020 decline (must reference the data).

- 1 mark for describing the recovery post-2020.

- Award marks only if the answer references Table 1 data. A generic description without data reference scores a maximum of 1 mark.

Question 2

With reference to Table 1, compare the share of manufacturing and services in Singapore's GDP from 2015 to 2023. [4]

Answer:

The services sector was the dominant sector throughout the period, accounting for over 70% of GDP in all years, ranging from a low of 70.2% in 2021 to a high of 73.8% in 2016. [1] Manufacturing contributed a smaller but significant share, ranging from 18.1% in 2016 to 22.3% in 2021. [1] While the services share showed a slight overall decline from 73.2% in 2015 to 71.5% in 2023, the manufacturing share increased slightly from 18.5% to 20.9% over the same period. [1] Notably, both sectors saw their shares move in opposite directions in 2020–2021, with manufacturing's share rising (to 21.5% and 22.3%) while services' share fell (to 71.0% and 70.2%), possibly reflecting pandemic-related shifts in economic activity. [1]

Marking Notes:

- 1 mark for describing the services sector share (must include data).

- 1 mark for describing the manufacturing sector share (must include data).

- 1 mark for comparing the trends (both direction and magnitude).

- 1 mark for identifying the notable divergence in 2020–2021 with data reference.

- Answers must use comparative language (e.g., "whereas," "in contrast," "while") to receive full marks.

Question 3

With reference to Table 2, compare the unemployment rate and median monthly income in Singapore from 2015 to 2023. [4]

Answer:

The unemployment rate and median monthly income generally moved in opposite directions over the period. [1] The unemployment rate rose from 1.9% in 2015 to a peak of 3.0% in 2020, before falling back to 2.0% in 2023. [1] Meanwhile, median monthly income rose consistently from S3,949in2015toS5,190 in 2023, with only a slight dip in 2020 to S$4,534. [1] Both indicators were affected by the pandemic in 2020, with unemployment rising and income falling slightly, but both recovered in subsequent years, with unemployment returning to near pre-pandemic levels and income continuing its upward trend. [1]

Marking Notes:

- 1 mark for identifying the inverse relationship between the two variables.

- 1 mark for describing the unemployment trend with data.

- 1 mark for describing the income trend with data.

- 1 mark for linking both to the pandemic impact and recovery.

- Answers must reference Table 2 explicitly.

Question 4

Using the data in Table 2, calculate the approximate percentage change in median monthly income from 2015 to 2023. Show your working. [2]

Answer:

Percentage change=Old valueNew value−Old value×100%

=39495190−3949×100%

=39491241×100%

≈31.4% [1]

Median monthly income increased by approximately 31.4% from 2015 to 2023. [1]

Marking Notes:

- 1 mark for correct formula and substitution.

- 1 mark for correct final answer (accept 31% to 31.5%).

- If the formula is wrong but the final answer is correct, award 1 mark.

- If only the final answer is shown without working, award 1 mark.

Question 5

With reference to Source C, identify two challenges Singapore faces in its economic transition. [2]

Answer:

- Vulnerabilities in sectors reliant on foreign labour and global supply chains, as exposed by the COVID-19 pandemic. [1]

- The rise of artificial intelligence and automation, which poses threats to mid-career workers in routine-intensive occupations. [1]

Marking Notes:

- 1 mark per valid challenge identified, up to 2 marks.

- Answers must be drawn from Source C. Generic answers not referenced to the source score 0.

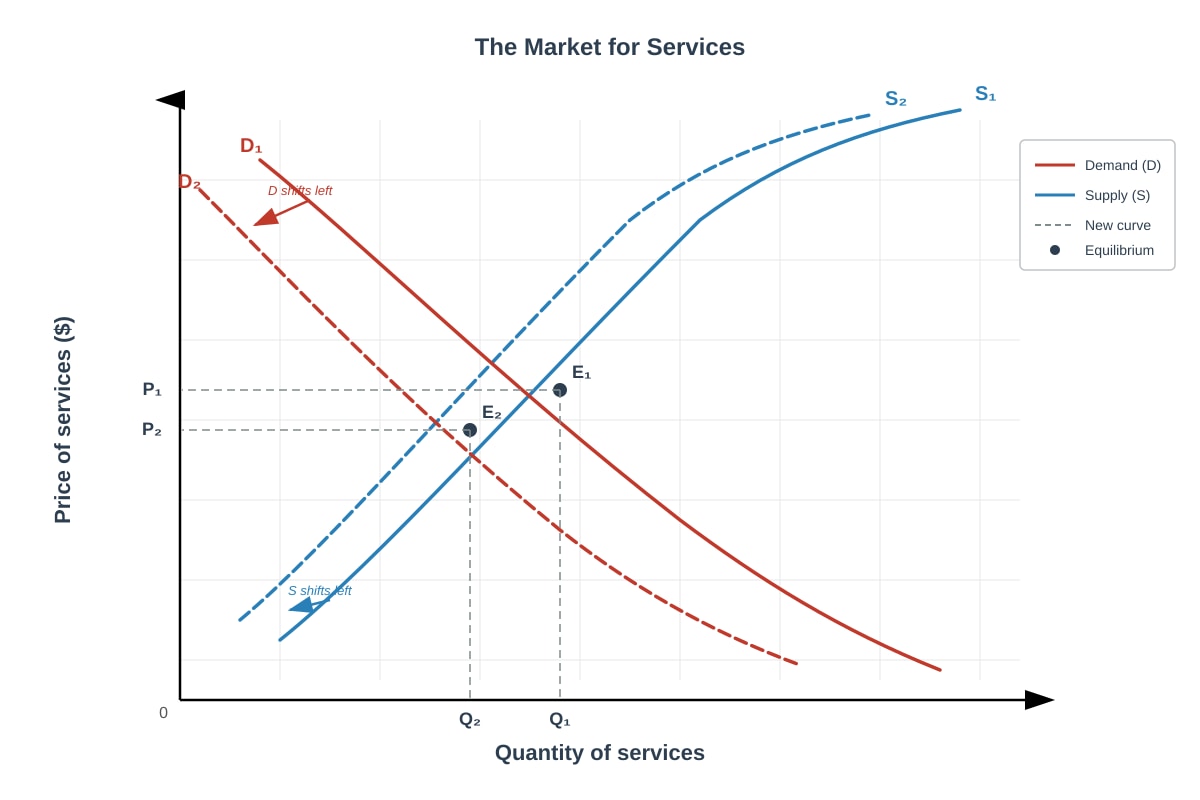

Question 6

Using a demand and supply diagram, explain how the COVID-19 pandemic in 2020 could have affected the equilibrium price and quantity of services in Singapore's economy. [5]

Answer:

The COVID-19 pandemic would have affected the services market through both demand and supply channels.

Demand-side: Lockdowns, social distancing measures, and reduced consumer confidence would have caused the demand curve for services to shift leftward (from D1 to D2), as consumers reduced spending on non-essential services such as tourism, dining, and entertainment. [1]

Supply-side: Restrictions on business operations, capacity limits, and workplace closures would have reduced the ability of firms to provide services, causing the supply curve to shift leftward (from S1 to S2). [1]

Diagram: The diagram should show both curves shifting leftward. The new equilibrium quantity (Q2) is unambiguously lower than Q1. The effect on price depends on the relative magnitude of the shifts. If the demand shift is larger than the supply shift, the equilibrium price falls from P1 to P2. [1]

<image_placeholder> id: Q6-fig1 type: diagram linked_question: Q6 description: A standard demand and supply diagram for the services market showing leftward shifts of both demand and supply curves, with the demand shift being larger than the supply shift, resulting in a lower equilibrium price and quantity. labels: D1, D2, S1, S2, E1, E2, P1, P2, Q1, Q2, Price of services ($), Quantity of services values: P1 > P2; Q1 > Q2; D2 left of D1; S2 left of S1; horizontal shift D1→D2 > horizontal shift S1→S2 must_show: Both demand and supply curves shifting leftward, original and new equilibrium points clearly labelled, axes labelled, arrows indicating direction of shift </image_placeholder>

Explanation: The pandemic caused both demand and supply of services to fall. The leftward shift in demand was likely greater than the supply shift for many service sectors (e.g., tourism, hospitality), leading to a fall in both equilibrium price and quantity. [1] The significant fall in output is consistent with the decline in Singapore's real GDP in 2020 shown in Table 1. [1]

Marking Notes:

- 1 mark for explaining the demand-side shift with economic reasoning.

- 1 mark for explaining the supply-side shift with economic reasoning.

- 1 mark for a correctly drawn and labelled diagram (both curves shifting left, correct equilibrium points).

- 1 mark for explaining the impact on equilibrium price and quantity.

- 1 mark for linking the analysis to the data in Table 1 or real-world context.

- The diagram must be clearly drawn with correct labels to earn the diagram mark. If the diagram is missing, award a maximum of 4 marks.

Question 7

Explain one reason why labour productivity growth was negative in 2020 and 2023, as shown in Table 2. [3]

Answer:

2020: Labour productivity growth was -0.5% in 2020 because the COVID-19 pandemic caused a sharp contraction in output (real GDP fell by about 5.6%), while firms retained workers due to government support measures such as the Jobs Support Scheme (JSS). [1] Since productivity is measured as output per worker, if output falls faster than the number of workers, productivity declines. [1]

2023: Labour productivity growth was -0.8% in 2023, possibly because firms were hiring and expanding their workforce in anticipation of recovery and growth, but the additional output from new workers had not yet materialised. [1] This is known as the "productivity J-curve" effect, where initial hiring of new workers temporarily reduces average productivity as new employees undergo training and onboarding.

Marking Notes:

- Award up to 2 marks for the 2020 explanation (1 for identifying the cause, 1 for explaining the mechanism).

- Award 1 mark for the 2023 explanation.

- Accept alternative valid explanations (e.g., structural shifts, measurement issues).

- The answer must demonstrate understanding of the concept of labour productivity (output per worker).

Question 8

Using the concept of income elasticity of demand, explain how the rise in median monthly income from 2015 to 2023 might affect the demand for different types of goods and services in Singapore. [5]

Answer:

Income elasticity of demand (YED) measures the responsiveness of quantity demanded to a change in income, ceteris paribus. It is calculated as:

YED=% change in income% change in quantity demanded

As median monthly income rose by approximately 31.4% from 2015 to 2023, the demand for different types of goods would be affected differently depending on their YED. [1]

Normal goods (YED > 0): For normal goods, an increase in income leads to an increase in demand. Normal necessities (0 < YED < 1), such as basic food items and utilities, would see a proportionally smaller increase in demand. For example, spending on groceries might increase, but not by as much as the rise in income. [1]

Superior/luxury goods (YED > 1): For luxury goods and services, such as overseas travel, fine dining, and premium healthcare, demand would increase by a proportionally greater amount than the rise in income. This is consistent with Singapore's growing expenditure on services such as tourism and healthcare as incomes have risen. [1]

Inferior goods (YED < 0): For inferior goods, such as low-cost instant meals or public transport (relative to private car ownership), demand would actually fall as consumers switch to higher-quality alternatives. [1]

Overall impact: The rise in income would lead to a change in the pattern of spending, with a greater proportion of income spent on services and luxury goods, and a smaller proportion on basic necessities and inferior goods. This is consistent with the structural shift towards a more service-oriented and consumption-driven economy in Singapore. [1]

Marking Notes:

- 1 mark for defining YED and/or stating the formula.

- 1 mark for explaining the impact on normal necessities with an example.

- 1 mark for explaining the impact on luxury goods with an example.

- 1 mark for explaining the impact on inferior goods with an example.

- 1 mark for linking the analysis to the Singapore context or overall spending pattern change.

- Award a maximum of 3 marks if no reference is made to the data in Table 2.

Question 9

Discuss whether the data in Tables 1 and 2 suggest that Singapore's economic strategy of moving up the value chain has been successful. [8]

Answer:

Introduction: Singapore's economic strategy of moving up the value chain involves shifting towards higher-value manufacturing and knowledge-intensive services, supported by investment in human capital and technology. The data in Tables 1 and 2 provide some evidence of success, but also reveal ongoing challenges.

Evidence suggesting success:

-

Rising real GDP: Real GDP grew from S423.8billionin2015toS515.7 billion in 2023, an increase of approximately 21.7%. This sustained growth suggests that the economy has been successful in generating higher-value output over time. [1]

-

Rising median income: Median monthly income rose from S3,949toS5,190, an increase of 31.4%, outpacing GDP growth. This suggests that the benefits of economic growth have been reflected in higher incomes for workers, consistent with a shift towards higher-value, higher-paying jobs. [1]

-

Labour productivity growth: Labour productivity growth was positive in most years (2017, 2018, 2021, 2022), indicating that output per worker was increasing — a key indicator of moving up the value chain. The 2021 figure of 5.4% was particularly strong. [1]

-

Manufacturing share resilience: The manufacturing sector's share of GDP remained relatively stable (18.5% to 20.9%), suggesting that Singapore has maintained its manufacturing base while also growing services — consistent with a dual strategy of high-value manufacturing and services. [1]

Evidence suggesting challenges:

-

Productivity volatility: Labour productivity growth was negative in 2020 (-0.5%) and 2023 (-0.8%), suggesting that the transition is not smooth and is vulnerable to external shocks and structural adjustments. [1]

-

Unemployment fluctuations: The unemployment rate rose to 3.0% in 2020, indicating that economic restructuring can lead to job displacement, particularly during crises. While it recovered to 2.0% by 2023, this highlights the ongoing challenge of ensuring that workers can transition to new roles. [1]

-

Services share decline: The services sector's share of GDP fell slightly from 73.2% to 71.5%, which might suggest that the shift towards knowledge-intensive services has not been as rapid as intended, or that manufacturing has become relatively more important. [1]

Conclusion: Overall, the data suggest that Singapore's strategy has been broadly successful, as evidenced by rising GDP, incomes, and generally positive productivity growth. However, the volatility in productivity and the challenges of economic restructuring indicate that the transition is ongoing and requires continued investment in reskilling and technology adoption. [1]

Marking Notes:

- This is an 8-mark question requiring a balanced discussion.

- Award up to 3 marks for identifying and explaining evidence of success (must reference data).

- Award up to 3 marks for identifying and explaining evidence of challenges (must reference data).

- Award up to 2 marks for a clear, well-reasoned conclusion that weighs the evidence.

- Answers must reference data from Tables 1 and 2 to earn marks. Generic answers without data reference score a maximum of 4 marks.

- For Level 3 (7–8 marks): Balanced discussion with data reference, clear analysis, and a well-supported conclusion.

- For Level 2 (4–6 marks): Some balance, limited data reference, basic analysis.

- For Level 1 (1–3 marks): One-sided or descriptive answer with little analysis.

Question 10

Evaluate the effectiveness of the Singapore government's policy of investing in human capital and reskilling programmes (as mentioned in Source C) in addressing structural unemployment. [10]

Answer:

Introduction: Structural unemployment occurs when there is a mismatch between the skills of workers and the requirements of available jobs, often due to technological change or shifts in the structure of the economy. The Singapore government's policy of investing in human capital and reskilling programmes, such as the SGUnited Jobs and Skills programme and SkillsFuture initiatives, aims to address this issue. This evaluation considers the effectiveness, limitations, and broader context of these policies.

How reskilling programmes address structural unemployment:

-

Reducing skills mismatch: By providing training in areas such as digital skills, data analytics, and advanced manufacturing, reskilling programmes help workers acquire the skills demanded by emerging industries. This directly addresses the root cause of structural unemployment — the skills gap. [1]

-

Supporting mid-career workers: Source C highlights the threat of AI and automation to mid-career workers in routine-intensive occupations. Programmes like SkillsFuture Credit and the Professional Conversion Programme (PCP) specifically target these workers, helping them transition to new roles and reducing the duration of unemployment. [1]

-

Improving labour productivity: A more skilled workforce is likely to be more productive, which is consistent with the generally positive labour productivity growth shown in Table 2 (e.g., 3.7% in 2018, 5.4% in 2021). Higher productivity supports economic growth and creates demand for skilled workers. [1]

Limitations and challenges:

-

Time lag: Reskilling programmes take time to design, implement, and produce results. Workers may remain unemployed or underemployed during the training period, and the skills taught may become outdated if the pace of technological change is rapid. [1]

-

Take-up and effectiveness: Not all workers may be willing or able to participate in reskilling programmes, particularly older workers or those with family responsibilities. The effectiveness of training also depends on its quality and relevance to actual job market needs. [1]

-

Demand-side factors: Reskilling alone cannot solve structural unemployment if there are insufficient job opportunities in the new industries. The government must also attract investment and create demand for skilled workers through industrial policy (e.g., incentives for high-tech manufacturing, support for the digital economy). [1]

-

Wage and cost considerations: Even with reskilling, workers may face lower wages in new industries compared to their previous roles, which could reduce the incentive to retrain. Additionally, the cost of reskilling programmes is borne by the government and taxpayers, raising questions about fiscal sustainability. [1]

Evaluation:

The policy is likely to be effective in the long run, as Singapore's strong economic fundamentals, targeted industrial policy, and high-quality education system provide a supportive environment. The recovery of the unemployment rate to 2.0% by 2023 (Table 2) suggests that the labour market has been resilient, and reskilling programmes have likely contributed to this. [1]

However, the policy is not a complete solution. It must be complemented by demand-side policies (e.g., attracting foreign direct investment, supporting entrepreneurship) and supply-side policies (e.g., immigration policy to fill skills gaps, education reform). The rise of AI and automation means that reskilling must be a continuous, ongoing process rather than a one-time intervention. [1]

Conclusion: Overall, investing in human capital and reskilling programmes is a necessary and largely effective policy for addressing structural unemployment in Singapore, but it is not sufficient on its own. Its effectiveness depends on the quality and relevance of training, the willingness of workers to participate, and the availability of job opportunities in new industries. A comprehensive approach combining reskilling with industrial policy and social support is needed. [1]

Marking Notes:

- This is a 10-mark evaluation question.

- Award up to 3 marks for explaining how reskilling addresses structural unemployment (with economic reasoning).

- Award up to 4 marks for discussing limitations and challenges (at least two well-developed points).

- Award up to 3 marks for a clear, balanced evaluation and conclusion.

- For Level 3 (8–10 marks): Comprehensive analysis, balanced evaluation, clear conclusion, data reference.

- For Level 2 (5–7 marks): Some analysis and evaluation, limited balance, basic conclusion.

- For Level 1 (1–4 marks): Descriptive or one-sided answer with little evaluation.

- Answers must reference Source C and/or Tables 1/2 to earn top-band marks.

Case Study 2: Global Trade, Inflation, and Policy Responses

Question 11

With reference to Table 3, compare the inflation rates of Singapore and the United Kingdom from 2019 to 2023. [4]

Answer:

Both Singapore and the United Kingdom experienced low inflation in 2019 (0.6% and 1.8% respectively), followed by a sharp increase in 2022 and a partial decline in 2023. [1] However, the UK's inflation rate was consistently higher than Singapore's in all years shown. [1] In 2022, the UK's inflation rate peaked at 9.1%, significantly higher than Singapore's 6.1%. [1] By 2023, both countries saw their inflation rates fall, but the UK's rate remained elevated at 7.3%, while Singapore's fell to 4.8%, suggesting that inflationary pressures were more persistent in the UK. [1]

Marking Notes:

- 1 mark for describing the common trend (low in 2019, peak in 2022, fall in 2023).

- 1 mark for noting that UK inflation was consistently higher.

- 1 mark for comparing the 2022 peak values with data.

- 1 mark for comparing the 2023 values and noting the difference in persistence.

- Answers must use comparative language and reference Table 3 data.

Question 12

With reference to Table 3, identify which country had the largest trade surplus in 2023 and suggest one reason for this. [3]

Answer:

Singapore had the largest trade surplus in 2023 at +US$58.3 billion. [1] One reason for this is Singapore's role as a major trading hub and entrepôt, with strong exports of electronics, pharmaceuticals, and refined petroleum products. Additionally, Singapore's strategic location and free trade agreements facilitate high volumes of trade. [1] Alternatively, Singapore's high current account surplus (17.6% of GDP) reflects its high savings rate and strong export competitiveness. [1]

Marking Notes:

- 1 mark for correctly identifying Singapore with the correct figure.

- 1 mark for a valid reason (accept any well-explained reason).

- 1 mark for linking the reason to economic concepts (e.g., comparative advantage, trade hub, savings-investment balance).

- Accept alternative valid reasons (e.g., strong manufacturing base, government trade policies).

Question 13

Using the data in Table 4, calculate the percentage change in the value of the Japanese Yen against the US Dollar from 2019 to 2023. Show your working. [2]

Answer:

In 2019, 1 US=109.0JPY.In2023,1US = 140.5 JPY. [1]

The JPY has depreciated against the US$. The percentage change is:

Percentage change=109.0140.5−109.0×100%

=109.031.5×100%

≈28.9% depreciation [1]

Marking Notes:

- 1 mark for correct substitution.

- 1 mark for correct final answer (accept 28.5% to 29%).

- The answer must state that the JPY depreciated (weakened) to earn the second mark.

- If the student calculates the change from the USD perspective (appreciation of USD), accept with correct working.

Question 14

With reference to Table 4, describe the trend in the exchange rate of the Singapore dollar against the US dollar from 2019 to 2023, and explain what this trend implies about the value of the Singapore dollar. [3]

Answer:

The exchange rate of the Singapore dollar against the US dollar showed a gradual appreciation from 2019 to 2023. The SGD strengthened from 1.36 SGD per USin2019to1.33SGDperUS in 2023, meaning that fewer Singapore dollars were needed to buy one US dollar. [1] This indicates that the Singapore dollar appreciated (increased in value) relative to the US dollar over this period. [1] This trend is consistent with MAS's policy of allowing a gradual and modest appreciation of the SGD to manage imported inflation, as described in Source F. [1]

Marking Notes:

- 1 mark for describing the trend with data reference.

- 1 mark for correctly stating that the SGD appreciated.

- 1 mark for linking the trend to MAS policy or Source F.

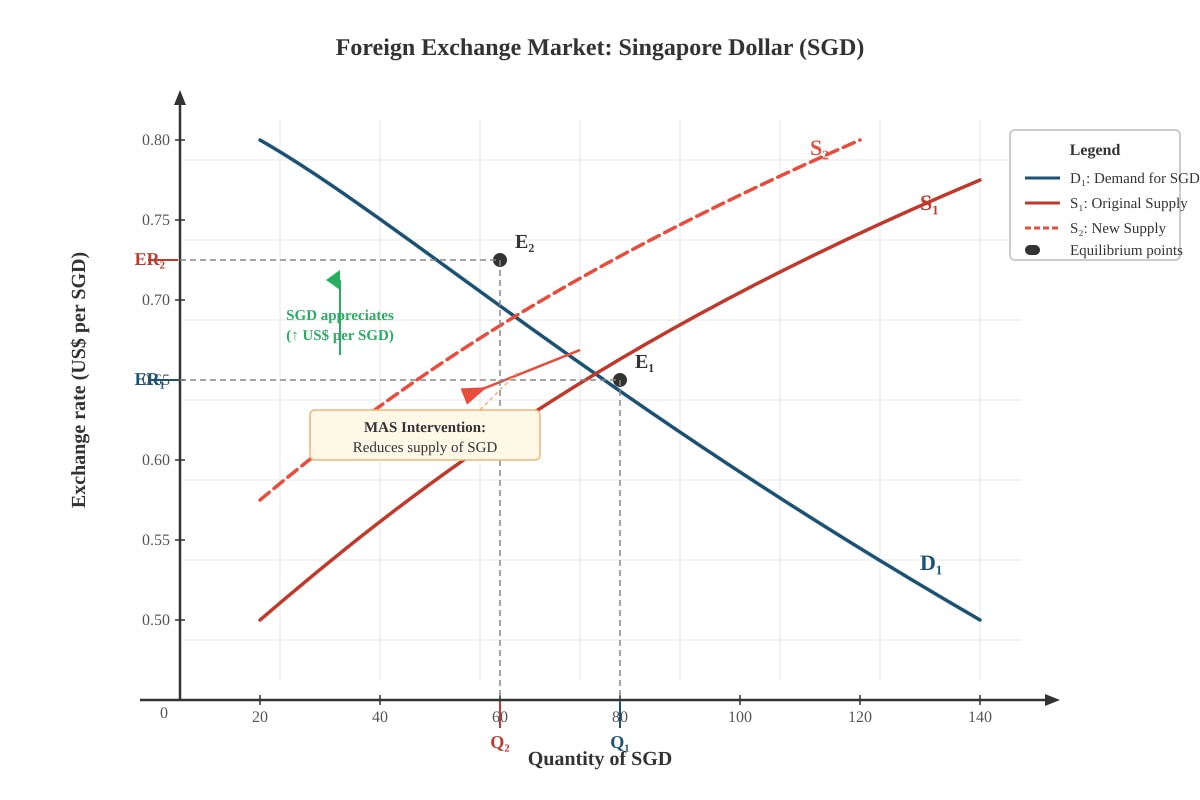

Question 15

Using a demand and supply diagram for the foreign exchange market, explain how MAS's policy of allowing a gradual appreciation of the Singapore dollar could be represented. [5]

Answer:

In the foreign exchange market, the exchange rate is determined by the demand for and supply of the Singapore dollar. MAS can influence the exchange rate by intervening in the foreign exchange market. [1]

To allow the SGD to appreciate, MAS would reduce the supply of SGD in the foreign exchange market (e.g., by buying SGD with foreign currency reserves). This shifts the supply curve of SGD leftward from S1 to S2. [1]

At the original exchange rate (ER1), the reduction in supply creates an excess demand for SGD, putting upward pressure on its value. The exchange rate rises from ER1 to ER2, meaning the SGD appreciates (more US$ per SGD). [1]

<image_placeholder> id: Q15-fig1 type: diagram linked_question: Q15 description: A demand and supply diagram for the Singapore dollar in the foreign exchange market, showing a leftward shift of the supply curve leading to a higher exchange rate (appreciation of SGD). labels: D1, S1, S2, E1, E2, ER1, ER2, Q1, Q2, Exchange rate (US$ per SGD), Quantity of SGD values: ER2 > ER1; Q2 < Q1; S2 is to the left of S1 must_show: Supply curve shifting leftward, original and new equilibrium points, axes clearly labelled, arrows showing direction of shift, the new exchange rate higher than the original </image_placeholder>

Explanation: The diagram shows that as the supply of SGD decreases (S1 to S2), the equilibrium exchange rate rises from ER1 to ER2, representing an appreciation of the SGD. The quantity of SGD traded falls from Q1 to Q2. [1] This is consistent with MAS's approach of managing the SGD through the trade-weighted exchange rate (SGD NEER) rather than interest rates. [1]

Marking Notes:

- 1 mark for explaining the foreign exchange market mechanism.

- 1 mark for explaining how MAS intervention reduces the supply of SGD.

- 1 mark for a correctly drawn and labelled diagram.

- 1 mark for explaining the impact on the exchange rate.

- 1 mark for linking to MAS policy or Source F.

- Award a maximum of 4 marks if the diagram is missing.

Question 16

Explain two possible causes of the high inflation rates observed in most countries in 2022, as shown in Table 3. [4]

Answer:

Cause 1: Cost-push inflation due to supply chain disruptions and the Russia-Ukraine conflict. [1] The Russia-Ukraine conflict, which began in February 2022, disrupted global supplies of energy (oil and natural gas) and food (wheat, sunflower oil), pushing up production costs for firms worldwide. This caused the short-run aggregate supply (SRAS) curve to shift leftward, leading to higher prices (cost-push inflation). This is consistent with the sharp rise in inflation in the UK (9.1%) and Singapore (6.1%) in 2022. [1]

Cause 2: Demand-pull inflation due to pent-up demand and expansionary policies. [1] During 2020–2021, many governments implemented expansionary fiscal and monetary policies (e.g., stimulus packages, low interest rates) to support their economies during the pandemic. As economies reopened in 2022, pent-up consumer demand, combined with excess liquidity, led to demand-pull inflation as the aggregate demand (AD) curve shifted rightward faster than aggregate supply could respond. This is particularly evident in the US, where inflation reached 8.0% in 2022. [1]

Marking Notes:

- 1 mark per cause identified (up to 2 marks).

- 1 mark per cause explained with economic reasoning and/or data reference (up to 2 marks).

- Accept alternative valid causes (e.g., loose monetary policy, wage-price spirals, depreciation of currencies increasing import costs).

- Answers must demonstrate understanding of inflation concepts (cost-push, demand-pull, AD-AS).

Question 17

Using the concept of price elasticity of demand, explain how a depreciation of the Malaysian Ringgit (as shown in Table 4) might affect Malaysia's trade balance. [5]

Answer:

From Table 4, the Malaysian Ringgit depreciated from 4.14 MYR per USin2019to4.56MYRperUS in 2023, a depreciation of approximately 10.1%. [1]

A depreciation of the Ringgit makes Malaysian exports cheaper in foreign currency terms and imports more expensive in domestic currency terms. The effect on the trade balance depends on the price elasticity of demand (PED) for exports and imports. [1]

If PED for exports and imports is relatively elastic (Marshall-Lerner condition holds): A depreciation would lead to a significant increase in export volumes (as foreign buyers respond to lower prices) and a significant decrease in import volumes (as domestic consumers switch to cheaper local alternatives). This would improve the trade balance. [1]

If PED for exports and imports is relatively inelastic: The increase in export volumes and decrease in import volumes would be small. In the short run, the trade balance might actually worsen (the J-curve effect) because the value of imports rises (more MYR needed to buy the same quantity of imports) before export volumes have time to adjust. [1]

Application to Malaysia: Malaysia's trade balance was +US$28.4 billion in 2023 (Table 3), suggesting a trade surplus. If the Marshall-Lerner condition holds (i.e., the sum of the PEDs for exports and imports is greater than 1), the depreciation of the Ringgit would help maintain or improve this surplus by making Malaysian exports more competitive. However, if demand is inelastic, the depreciation could initially worsen the trade balance before improving it over time. [1]

Marking Notes:

- 1 mark for calculating or stating the depreciation with data reference.

- 1 mark for explaining the effect of depreciation on export and import prices.

- 1 mark for explaining the Marshall-Lerner condition.

- 1 mark for discussing the J-curve effect (short-run vs long-run).

- 1 mark for applying the analysis to Malaysia's trade balance data.

- Award a maximum of 3 marks if the answer does not reference Table 3 or Table 4 data.

Question 18

Discuss whether the data in Tables 3 and 4 suggest that exchange rate movements are the main determinant of a country's trade balance. [8]

Answer:

Introduction: The trade balance is the difference between a country's exports and imports of goods and services. While exchange rate movements can influence the trade balance by affecting the relative prices of exports and imports, the data in Tables 3 and 4 suggest that other factors also play a significant role.

Evidence that exchange rates matter:

-

Singapore: The SGD appreciated slightly from 1.36 to 1.33 per US(2019–2023),yetSingaporemaintainedalargetradesurplus(+US58.3 billion in 2023). This suggests that exchange rate movements are not the only determinant — Singapore's trade surplus is also driven by its role as a trading hub, strong export competitiveness in high-value goods, and strategic trade policies. [1]

-

Japan: The JPY depreciated significantly from 109.0 to 140.5 per US(adepreciationofapproximately28.915.1 billion in 2023. If exchange rates were the main determinant, the depreciation should have improved Japan's trade balance by making exports cheaper and imports more expensive. The fact that Japan still has a deficit suggests that structural factors (e.g., high import dependence on energy, declining export competitiveness in some sectors) are more important. [1]

-

Malaysia: The MYR depreciated from 4.14 to 4.56 per US,andMalaysiahadatradesurplusof+US28.4 billion. The depreciation may have helped maintain the surplus by keeping exports competitive, but Malaysia's surplus is also driven by its commodity exports (palm oil, petroleum) and manufacturing exports. [1]

Evidence that other factors are important:

-

Structural factors: A country's trade balance depends on its comparative advantage, the diversity of its export base, and its dependence on imports. Singapore's high current account surplus (17.6% of GDP) reflects its high savings rate and strong export sector, not just exchange rate policy. [1]

-

Global demand conditions: The trade balance depends on the economic conditions of trading partners. Strong global demand for electronics and pharmaceuticals benefits Singapore and Malaysia, regardless of exchange rate movements. [1]

-

Terms of trade: Changes in the prices of a country's exports relative to its imports (terms of trade) can affect the trade balance independently of exchange rate movements. For example, rising commodity prices can improve the trade balance of commodity exporters like Malaysia. [1]

Conclusion: While exchange rate movements do influence the trade balance, the data suggest that they are not the main determinant. Structural factors, global demand conditions, terms of trade, and domestic economic policies all play important roles. The relationship between exchange rates and the trade balance is complex and depends on the price elasticities of demand for exports and imports (Marshall-Lerner condition), as well as the time horizon considered. [1]

Marking Notes:

- This is an 8-mark discussion question.

- Award up to 3 marks for analysing the relationship between exchange rates and trade balance using data from Tables 3 and 4.

- Award up to 3 marks for discussing other determinants of the trade balance.

- Award up to 2 marks for a clear, well-reasoned conclusion.

- For Level 3 (7–8 marks): Balanced discussion with extensive data reference, clear analysis, and a well-supported conclusion.

- For Level 2 (4–6 marks): Some balance, limited data reference, basic analysis.

- For Level 1 (1–3 marks): One-sided or descriptive answer with little analysis.

Question 19

Explain how MAS's exchange rate-based monetary policy helps Singapore manage imported inflation, as described in Source F. [5]

Answer:

Singapore is a small, open economy where imports constitute a significant share of consumption and production inputs. This means that changes in import prices have a large impact on domestic inflation. [1]

MAS manages monetary policy through the trade-weighted exchange rate (SGD NEER) rather than through interest rates. By allowing a gradual appreciation of the Singapore dollar, MAS makes imports cheaper in domestic currency terms. [1]

When the SGD appreciates, each unit of SGD can buy more foreign currency, which means that the SGD price of imported goods and services falls. For example, if the price of imported oil is US80perbarrelandtheexchangeratemovesfrom1.40SGD/US to 1.33 SGD/US,theSGDpriceofoilfallsfromS112 to S$106.40, reducing cost-push inflationary pressures. [1]

This is particularly important during periods of high global inflation, such as 2022–2023, when global supply chain disruptions and the Russia-Ukraine conflict pushed up energy and food prices worldwide. By tightening monetary policy through a steeper slope of the SGD NEER policy band (as MAS did on four occasions between October 2021 and October 2022), MAS helped to moderate the pass-through of global price increases to domestic inflation. [1]

The effectiveness of this policy depends on the proportion of imports in the consumer basket and the degree to which exchange rate changes are passed through to domestic prices. For Singapore, where imports account for a large share of consumption, exchange rate policy is a relatively effective tool for managing imported inflation. [1]

Marking Notes:

- 1 mark for explaining Singapore's dependence on imports.

- 1 mark for explaining how SGD appreciation reduces import prices.

- 1 mark for providing a numerical example or clear illustration.

- 1 mark for linking to the 2022–2023 context and MAS policy actions.

- 1 mark for evaluating the effectiveness or limitations of the policy.

- Award a maximum of 3 marks if the answer does not reference Source F.

Question 20

Evaluate the extent to which a small, open economy like Singapore can use monetary policy to control inflation without significantly harming its economic growth. [10]

Answer:

Introduction: Singapore's unique monetary policy framework — managing the trade-weighted exchange rate (SGD NEER) rather than interest rates — reflects the realities of a small, open economy where trade exceeds 300% of GDP. This evaluation considers the effectiveness, trade-offs, and limitations of using exchange rate policy to control inflation while maintaining economic growth.

How exchange rate policy controls inflation:

-

Managing imported inflation: As explained in Source F, a stronger SGD reduces the domestic price of imports, which is particularly important for Singapore given its heavy reliance on imported food, energy, and intermediate goods. This helps to contain cost-push inflation. [1]

-

Anchoring inflation expectations: A credible exchange rate policy can help anchor inflation expectations, reducing the risk of wage-price spirals and second-round inflationary effects. [1]

Trade-offs and potential harm to growth:

-

Export competitiveness: A stronger SGD makes Singapore's exports more expensive in foreign currency terms, potentially reducing export demand and harming economic growth. This is particularly relevant for Singapore's manufacturing and services sectors, which are heavily export-oriented. Table 1 shows that manufacturing accounted for about 20% of GDP, so a significant loss of export competitiveness could have a material impact on growth. [1]

-

Attracting foreign investment: While a strong currency signals economic stability, an excessively strong SGD could deter foreign direct investment (FDI) by increasing the cost of setting up operations in Singapore. [1]

-

Limited control over domestic inflation: Exchange rate policy is effective at managing imported inflation but may be less effective at controlling domestically generated inflation (e.g., from wage increases or property price bubbles). In such cases, the government may need to rely on supplementary measures such as fiscal policy or macroprudential regulations. [1]

Effectiveness in the Singapore context:

-

High import dependence: Given Singapore's extreme openness to trade, exchange rate policy is a more effective tool for managing inflation than interest rates, which would have limited domestic impact but could create distortions in asset markets. [1]

-

Complementary policies: Singapore's government uses a combination of monetary policy (exchange rate), fiscal policy (e.g., targeted subsidies, GST vouchers), and supply-side policies (e.g., increasing food diversification, investing in productivity) to manage inflation without relying solely on the exchange rate. This multi-pronged approach reduces the burden on any single policy tool. [1]

-

Credibility and flexibility: MAS's track record of managing the SGD NEER provides credibility, and the ability to adjust the slope, width, and centre of the policy band allows for flexibility in responding to changing economic conditions. [1]

Evaluation:

The evidence from Table 3 shows that Singapore's inflation rate fell from 6.1% in 2022 to 4.8% in 2023, while real GDP continued to grow (Table 1: from S503.1billionin2022toS515.7 billion in 2023). This suggests that MAS's tightening of monetary policy was effective in moderating inflation without causing a recession. [1]

However, the relationship is not without trade-offs. The appreciation of the SGD may have contributed to slower export growth in some sectors, and the full effects of monetary tightening may take time to materialise. Additionally, Singapore's small and open economy means that it is highly vulnerable to external shocks (e.g., global recessions, geopolitical conflicts) that are beyond the control of domestic monetary policy. [1]

Conclusion: Overall, Singapore's exchange rate-based monetary policy is a relatively effective tool for controlling inflation without significantly harming economic growth, particularly given the country's high import dependence and openness to trade. However, it is not a panacea, and its effectiveness depends on the nature of inflationary pressures (imported vs. domestic), the responsiveness of trade flows to exchange rate changes, and the use of complementary fiscal and supply-side policies. A balanced approach that considers both inflation and growth objectives is essential. [1]

Marking Notes:

- This is a 10-mark evaluation question.

- Award up to 3 marks for explaining how exchange rate policy controls inflation.

- Award up to 3 marks for discussing trade-offs and potential harm to growth.

- Award up to 2 marks for evaluating effectiveness in the Singapore context.

- Award up to 2 marks for a clear, balanced conclusion with data reference.

- For Level 3 (8–10 marks): Comprehensive analysis, balanced evaluation, clear conclusion, extensive data reference.

- For Level 2 (5–7 marks): Some analysis and evaluation, limited balance, basic conclusion.

- For Level 1 (1–4 marks): Descriptive or one-sided answer with little evaluation.

- Answers must reference Source F and/or Tables 1, 3, and 4 to earn top-band marks.

Mark Summary

| Question | Marks |

|---|---|

| Q1 | 3 |

| Q2 | 4 |

| Q3 | 4 |

| Q4 | 2 |

| Q5 | 2 |

| Q6 | 5 |

| Q7 | 3 |

| Q8 | 5 |

| Q9 | 8 |

| Q10 | 10 |

| Q11 | 4 |

| Q12 | 3 |

| Q13 | 2 |

| Q14 | 3 |

| Q15 | 5 |

| Q16 | 4 |

| Q17 | 5 |

| Q18 | 8 |

| Q19 | 5 |

| Q20 | 10 |

| Total | 95 |

Note: This practice paper is marked out of 95. In an actual H1 Economics examination, the total would be scaled to 100 marks.

Free quiz and exam paper access

Enter your details to view this paper

Your access is remembered on this device.